The rollout of coronavirus vaccines provides some hope that the worst effects of the pandemic will subside in 2021, although measures to contain the virus are expected to remain in place for some time yet. However, the economic, political and societal consequences of the pandemic are likely to be a source of heightened business interruption risk in the years ahead.

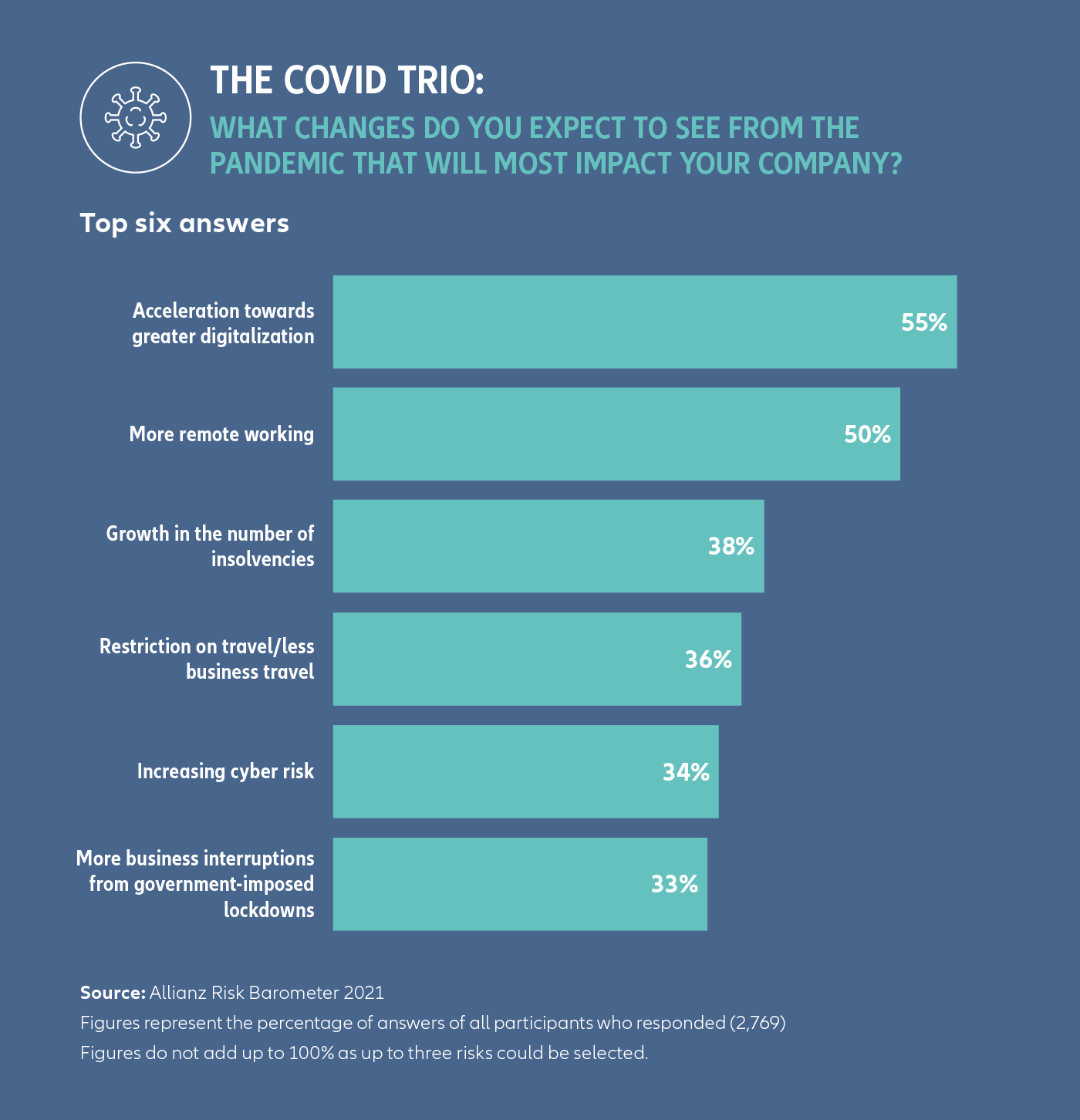

When asked which change caused by the pandemic will most impact businesses, Allianz Risk Barometer respondents cited the acceleration towards greater digitalization, followed by more remote working, growth in the number of insolvencies, restrictions on travel/ less business travel and increasing cyber risk. All these consequences will influence business interruption risks in the coming months and years

The knock-on effects of the pandemic can also be seen further down the rankings in this year’s Risk Barometer. A number of the climbers in 2021 – such as market developments, macroeconomic developments and political risks and violence – are in large part a consequence of the coronavirus outbreak. For example, the pandemic was accompanied by civil unrest in the US related to the Black Lives Matter movement, while anti-government protest movements simmer in parts of Latin America, Middle East and Asia, driven by inequality and a lack of democracy.

“Disruption associated with political, economic and social trends, like strikes, protests and civil unrest, is often underestimated. The economic consequences of the pandemic could fuel further political and social unrest in 2021 and beyond, with potential implications for supply chains and business interruption,” says Beblo.

Rising insolvency rates could also affect supply chains. According to Euler Hermes [2], the bulk of insolvencies will come in 2021. The trade credit insurer’s global insolvency index is expected to hit a record high for bankruptcies, up 35% by the end of 2021, with top increases expected in the US, Brazil, China and core European countries such as the UK, Italy, Belgium and France. Fraud and theft have also been on the rise during the pandemic, as criminals take advantage of business disruption and lax security. “The direct effects of the pandemic could recede in 2021 but the consequences of Covid-19 will be with us for some time after,” says Beblo. “The economic effects of coronavirus could affect demand while suppliers could file for bankruptcy. Cyber risks will also be a more significant source of business interruption risk going forward, as the pandemic has hastened digitalization and remote working.”

“Displaced workforces create new opportunities for increasingly well-organized and funded cyber criminals to exploit and gain access to networks and sensitive information,” says Georgi Pachov, Head of Portfolio Steering and Pricing at AGCS. “At the same time the potential impact from human error or technical failure incidents – already one of the most frequent drivers of cyber insurance claims – may also be heightened.”